Classification of Inventories

Merchandise vs. Manufacturing Company

Merchandise Company:

- Inventory

–> Current Asset

Manufacturing Company

- Raw Materials

- Work in Process

- Finished Goods

–> Current Asset

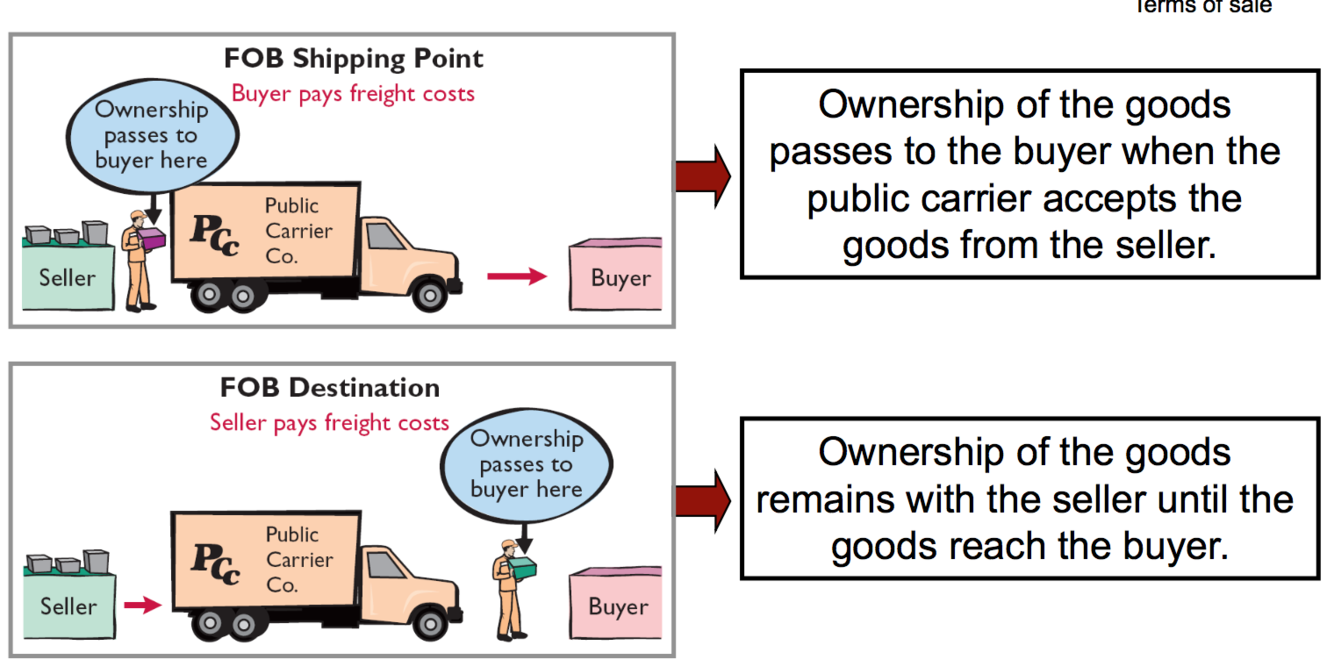

Determine Ownership of Goods:

Goods in Transit

- Purchased Goods not yet received

- Sold goos not yet delivered

Goods in transit should be included in the inventory of the company that has a LEGAL TITLE to the goods.

Legal Title

Is Determined by the terms of sale

Determining Ownership of Goods:

Consigned Goods

- Goods held for sale by one party

- Ownership of the goods is retained by another party

Name Three Inventory Costing Methods

- Specific Identifciation

- FIFO

- Average-Cost

Inventory Method

Specific Identification

- Actual Physical Flow Costing method

- Each item is specifically costed

Question: Does COST FLOW need to be consistent with PHYSICAL MOVMENT of the goods

NO!!!

FIFO

- First In First Out

- Earliest goods purchased are first to be sold

- Parallels actual physcial flow of merchandies

Average Cost

+ Formel

- Allocates cost of goos avaiable for sale on the basis of weighted-average units cost incurred

- Assumes goods are similar in nature

- Applies weighted-average unit cost to the units on hand to determine cost of the ending inventory

COGS Formular

Beginning Inventory

+ Cost of Goods Purchased

- Ending Inventory

= COGS

Inventory Turnover

= COGS / Average Inventory

- measures the number of times on average the inventory is sold during the period

- Purpose:

- to measrue the liquidity of the inventory

Days in Inventory

= Days in a YEAR (365) / Inventory Turnover

- measures the average number of days inventory is held (before it’s sold)

Cost Flow Assumption

- Assume flows of costs that may be unrelated to the physical flow of goods

- FIFO

- Average Cost

- There is NO accounting requirement that the cost flow assumption be consistent with the physical movement of the goods

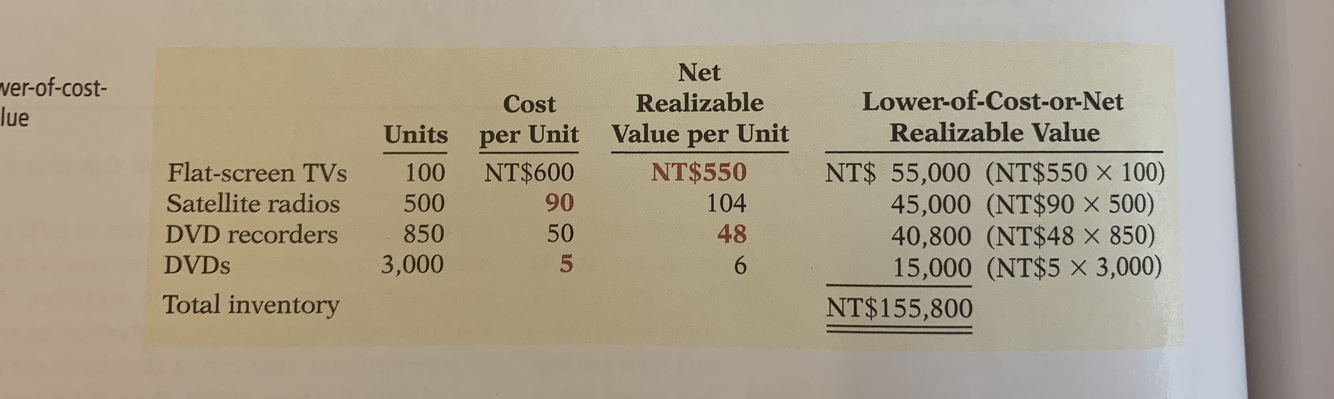

Lower-of-Cost-or-Net Realizable Value

Niederstwertrpinzip

- When the value of Inventory is lower than its cost, companies must “write down” the inventory to its net realizable value

- This is done by valuing the inventory at the lower-of-cost-or-net realizable value in the period in which the price decline occurs

- At NET REALIZABLE VALUE

Net Realizable Value

- Amount that a company expects to realize/receive from the sale of inventory

Estimated Selling Price

- Estimated Cost to complete and sell

Income Statement Effect

Inventory Error

- Affect the computation of COGS and NET Income

- in TWO PERIODS

- An error in ending Inventory of the current period will have a reverse effect on net incoome of the next accounting period

- Over the two year, the total net income is corrected because the errors offset each other