If inventory is sold with terms of FOB destination, the goods belong to the seller until they reach their destination.

TRUE The title to the goods transfers to the buyer at the destination when the terms are FOB destination

- In each accounting period, a manager can select the inventory costing method that yields the most positive net income.

FALSE A change in inventory method is allowed only if it will improve the accuracy with which financial results and financial position are measured.

A company’s ability to pay its short-term obligations depends on many factors including how quickly it sells its inventory.

TRUE How quickly inventory is sold to customers and cash is collected are factors in determining a company’s ability to pay its short-term obligations.

- The choice of an inventory costing method can have a major impact on gross profit and cost of goods sold.

TRUE The four inventory costing methods produce different results for cost of goods sold, and as a result, can have a major impact on gross profit.

- The understatement of beginning inventory balance causes cost of goods sold to be understated and net income to be understated.

FALSE Beginning inventory is added in the equation to determine cost of goods sold, so if it is understated, then cost of goods sold is understated. If the cost of goods sold expense on the Income Statement is understated, then net income will be overstated.

- Carrying insufficient quantities of inventory on hand: A. can inadvertently lower a company’s costs so much that its taxes become excessive. B. can cause customers to go elsewhere to obtain the product. C. has little effect on customer satisfaction. D. will increase the costs of carrying inventory.

B. can cause customers to go elsewhere to obtain the product. Customers’ needs will not be satisfied by the company so they will go elsewhere.

- The primary goals of inventory management do not include: A. maintaining a sufficient quantity of inventory to keep customers satisfied. B. maintaining sufficient quality of inventory to keep customers satisfied. C. minimizing the costs associated with maintaining inventories. D. purchasing inventory that will not be sold soon after they are acquired

D. purchasing inventory that will not be sold soon after they are acquired

- Which of the following is the equation for cost of goods sold? A. Beginning inventory + net purchases - Ending inventory B. Beginning inventory + net purchases + Ending inventory C. Net purchases - Beginning inventory D. Ending inventory + net purchases - Beginning inventory

A. Beginning inventory + net purchases - Ending inventory Beginning inventory + net purchases = goods available for sale Goods available for sale - Ending inventory = Cost of goods sold

- A merchandise company’s beginning inventory plus merchandise purchases equals: A. ending inventory. B. cost of goods sold. C. goods available for sale. D. sales level.

C. goods available for sale. Goods available for sale = Beginning inventory + Net purchases

- A merchandise company’s beginning inventory plus merchandise purchases minus ending inventory equals: A. ending inventory. B. cost of goods sold. C. goods available for sale. D. sales level.

B. cost of goods sold. Beginning inventory + net purchases = goods available for sale Goods available for sale - Ending inventory = Cost of goods sold

- If a company purchased 200 units of inventory at $9 per unit and 300 units at $10 per unit, its weighted average unit cost for this inventory would be: A. $9.00. B. $9.50. C. $9.60. D. $10.00.

C. $9.60.

- Which of the following accounts would normally have a credit balance? A. Inventory B. Cost of goods sold C. Sales D. Sales returns & allowances

C. Sales

Sales is a revenue account which has a normal credit balance.

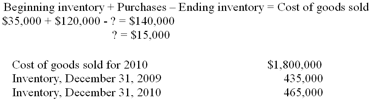

- If a firm’s beginning inventory is $35,000, goods purchased during the period cost $120,000, and the cost of goods sold for the period is $140,000, what is the amount of the ending inventory? A. $45,000 B. $20,000 C. $25,000 D. $15,000

D. $15,000

- The aging of accounts receivable method is based upon the principle that the longer an account is overdue, the higher the risk of nonpayment.

TRUE

Historical experience has shown that the longer an account remains unpaid, the higher the probability that it will never be paid.

- The receivables turnover ratio is calculated using the average net receivables.

TRUE

Receivables turnover ratio = Net Sales/Average Net Receivables.

- Allowance for doubtful accounts is a temporary account which is closed to retained earnings at the end of the accounting period.

FALSE

The allowance for doubtful accounts is a permanent account.

- The use of the Allowance method is required under the matching principle.

TRUE

An estimate of the amount of accounts receivable which will not be collected is necessary to achieve matching of revenues and expenses.

- Neither GAAP nor IFRS allow the use of the direct write-off method.

TRUE

GAAP and IFRS do not approve the use of the direct write-off method.

- The percentage of credit sales method, also called the income statement approach, estimates bad debts based on a historical percentage of sales that lead to bad debt losses.

TRUE

Bad debts expense is calculated as a % of credit sales reported on the income statement.

- A company extends credit to customers because it expects the: A. rise in sales revenue to be greater than the rise in cost of extending credit. B. delay in receiving cash to cost more than the increase in wage costs. C. tax savings from a lower net income to be greater than the cost of extending credit. D. bad debts expense to be less than the additional wage costs.

A. rise in sales revenue to be greater than the rise in cost of extending credit.

A company extends credit if it believes the additional revenues will exceed the additional costs.

- If a company did not extend credit to customers: A. gross revenue would rise. B. costs would rise but so would its revenue. C. costs would fall but so would its revenue. D. gross profit would rise.

C. costs would fall but so would its revenue.

Extending credit to customers generally increases sales and introduces additional costs such as increased wage costs and bad debt costs; therefore, a company that does not extend credit will have less revenue and fewer costs.

- An allowance for doubtful accounts is a contra-account paired with: A. expenses. B. cash. C. net income. D. accounts receivable.

D. accounts receivable.

The balance sheet reports net accounts receivable in the asset section which is calculated as accounts receivable minus the allowance for doubtful accounts.

- Net accounts receivable is: A. gross accounts receivable minus cost of goods sold. B. also known as net pretax income. C. gross accounts receivable minus allowance for doubtful accounts. D. also known as net after-tax income.

C. gross accounts receivable minus allowance for doubtful accounts.

Accounts receivable minus the contra-asset account, Allowance for doubtful accounts, equals net accounts receivable.

- On the balance sheet, the allowance for doubtful accounts: A. is included in current liabilities. B. increases the reported net value of accounts receivable. C. appears under the heading “Other Assets.” D. is deducted from accounts receivable.

D. is deducted from accounts receivable.

The balance sheet assets include net accounts receivable which is accounts receivable minus the allowance for doubtful accounts.