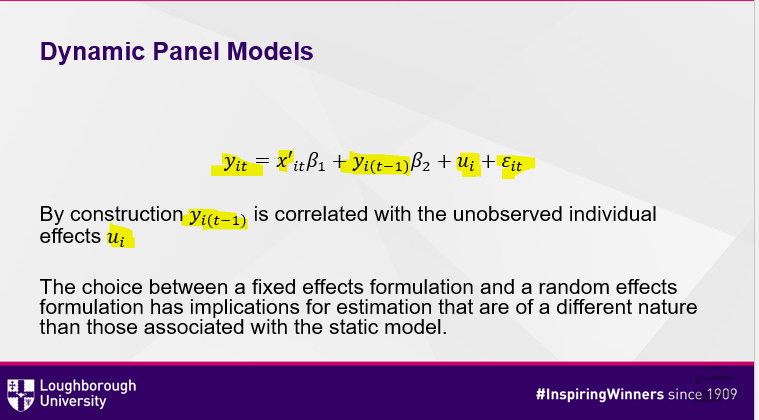

What are Dynamic Panel Models?

- Model in which the lag of the dependent variable is included in the current set of explanatory variables

- Current behaviour is modelled of previous behaviour

Why is the choice between fixed and random effect formulation important for the implication for estimation for Dynamic rather than static panel models?

- normal (static) model

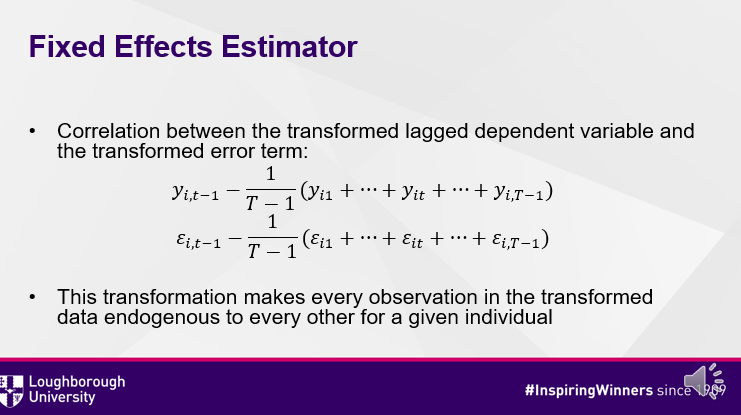

- In the normal fixed effect, the transformation would aggregate the dependent variable, across all individuals, and average them across time –> then subtracted from every term

- and so would the error term

- The problem with this transformation is that it makes every observation in the transformed data set endogenous to every other for a given individual

How do we go about finding the fixed effect of a dynamic panel model?

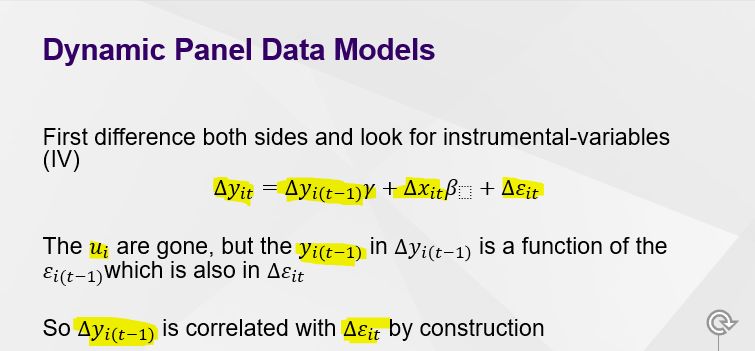

- Taking first differences allows us to remove the unobserved individual effect but now the problem that the lagged of the dependent variable ‘y’ is now a part of both the explanatory and dependent variables of the delta transformed equation.

- This means that ∆yi(t-1) is correlated with ∆εit by contruct.

*

- This means that ∆yi(t-1) is correlated with ∆εit by contruct.

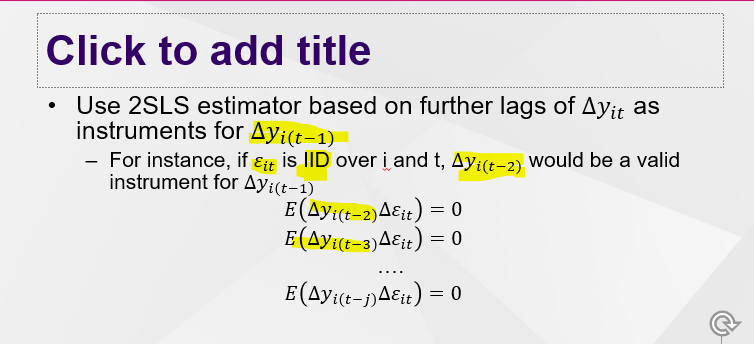

How do we solve the endogeneity problem caused by the first difference transformation of a dynamic panel data model?

- As long as the error term is Independent and individually distributed across i (cross-sectional units) and t (time-series dimension)

- Further lags could be used as an instrument as they will not be correlated with the error term

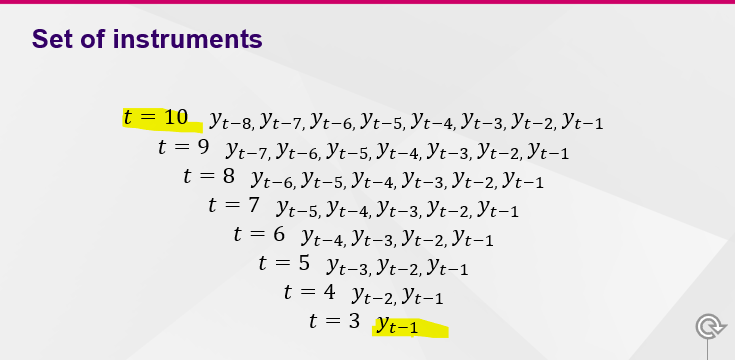

How many instruments should we use the the 2SLS estimation of the dynamic panel model?

- For static random-effects model estimation:

- Two period were enough

- For dynamic models:

- Will now need a minimum of three period of time (due to the inclusion of the lagged variable in the first difference transformation)

- So if we have three period of time –> we can have one instrument

- The more period of the we have the more instrument we have access to

- Will now need a minimum of three period of time (due to the inclusion of the lagged variable in the first difference transformation)

What other estimator can we use for Dynamic Panel Models?

- Very Similar to 2SLS estimation

- GMM also allows for heteroscedasticity and autocorrelation within individual units error but not across them all

- •‘small T’ and ‘large N’ panels; –> suitable for micro panels

- •A linear function relationship;

- •Dynamic left-hand side variable; –> lagged dependent variable being included as an explanatory variable

- •Endogenous right-hand side variables; –> due to the pervious point

- •Fixed individual effects;

- •Heteroscedasticity and autocorrelation within individual units errors but not across them.

What is the first type of GMM model?

•The difference GMM approach deals with this inherent endogeneity by transforming the data to remove the fixed effects.

The standard approach applies the first difference (FD) transformation, which removes the unobserved fixed effect at the cost of introducing a correlation between ∆y(i,t-1) and the difference error term(∆vit,) both of which have a term dated (t − 1).

This is preferable to the application of the within transformation, as that transformation makes every observation in the transformed data endogenous to every other for a given individual.

This is the first step, after which we will look for instruments

What is the other type of GMM models?

- Difference GMM

- First differenced variables are instrumented with lagged levels

- System GMM

- Augments ‘difference GMM’ by estimating simultaneously in differences and levels, the two equations being distinctly instrumented –> levels of instrumented with differences while differences are instrumented with levels

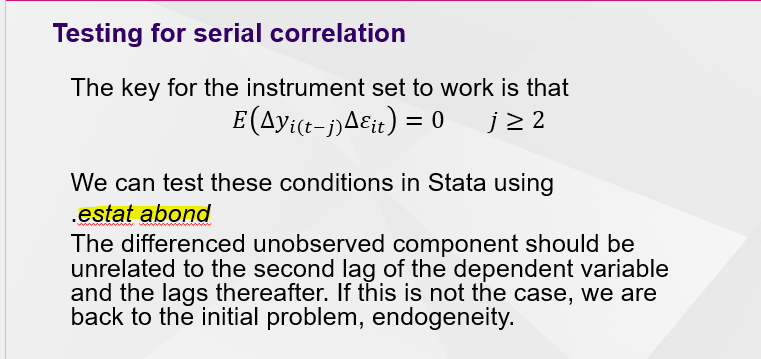

What do we need to test for to make sure our instruments chosen are appropriate for the model?

- •By construction (first differencing) , the residuals of the differenced equation should possess serial correlation

- (hence the lagged dependent variable needs to be instrumented from the endogeneity introduced form differing to get rid of the unoberserved heterogeneity)

- , but the differenced residuals should not exhibit significant AR(2) behaviour. If a significant AR(2) statistic is encountered, the second lags of endogenous variables will not be appropriate instruments for their current values.

- •Potential solution: limit the number of lags to be included as instruments.

How do we test if the second-order lags and further are serially correlated via Stata?

- Before we instrument the endogenous transformed lagged dependent variable on the right-hand side we need to make sure the the difference first component is unrelated to the second lag of the depdent variable and the lags thereafter

What is the Sargan/Hansen test?

- the 2nd thing that needs to be tested for in dynamic panel data is the validity of instruments used

- The Sargan/Hansen test is used to test the validity of the instruments whether they exogenous or whether they are correlated with the error term

- •A crucial assumption for the validity of GMM is that the instruments are exogenous.

- •Sargan/Hansen test statistics is itself asymptotically χ2, with degrees of freedom equal to the number of suspect instruments.

- H0: the instruments are valid.

-

L1 - Introduction to Time Series5

-

L2 - Stationary Processes42

-

L3 - Non-stationary Processes25

-

L4 - Co-integration and ECM20

-

L5 - VARs and VECMS23

-

L6 - (PL) Binary Choice Models14

-

L6 - Binary Choice Models12

-

L7 - (PL) Multinomial and Ordered Choice Models12

-

L8 - Multinomial Choice Models17

-

L9 - Ordered Choice Models15

-

L10 - (PL) Introduction to Panel Data Models5

-

L11 - (PL) Endogeneity and IV Estimator12

-

L12 - Panel Data Econometrics15

-

L13 - Dynamic Panel Data Models11