Diagram of Models Tested

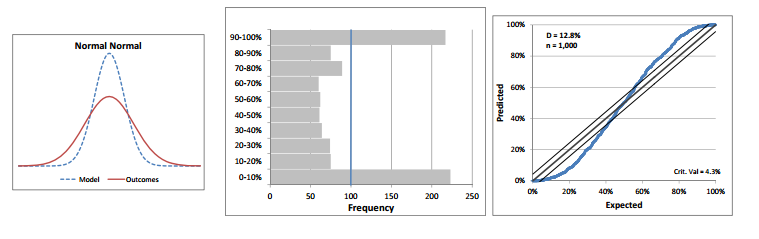

Kolmogorov-Smirnov (KS) Test

D=max |pi-ei|

Reject the null hypothesis (predicted percentiles are normal) if D>136/n.5

LIght Tailed Distributions

Heavy Tailed Distributions

Biased High/Upward

Diagnostics

What to look for in the p-p plots

Slope at the right tail & left tail

Shallow Slope indicates the model has a light tail

Steep Slope indicates that model has a heavy tail

Predicted Percentiles are accepted as uniform unless they fail the KS Test at the 5th percentile

Two metrics to test stability in the book of business

- Consistency in net earned premium

- Consistency in the ratio (Net Premium/Direct Premium)

Mack (Incurred)

- Fits a mean & standard deviation to the unpaid losses for each AY

- Overall:

- Light left tail

- Very light right tail

- Fails KS test

- Need to look for a predictive distribution that has fatter tails

Leveled Chain Ladder (Incurred) - LCL

- Add “column” correlation - Treat the value at the last diagonal for the row as a random variable

- u(w,d) = alpha(w) + b(d)

- Has more variance than Mack

- Overall:

- Definite light tails

- Fails KS test

- Improvement over Mack but still forecasts tails that are too light

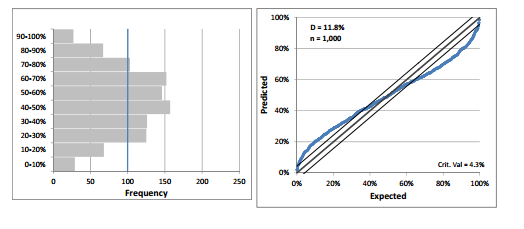

Correlated Chain Ladder (Incurred) - CCL

- Continue to use “column” correlation

- Add a parameter p to create correlation of losses by AY

- u(w,d) = alpha(w) + b(d) +p(ln(C(w-1,d) - u(w-1,d))

- More variance than Mack

- Overall:

- Very slight light tails on both sides

- Passes KS test

- Meyers concludes this model is good enough

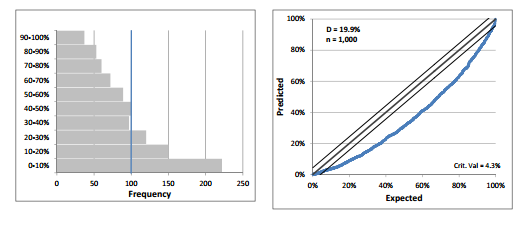

ODP Bootstrap (Paid)

- Overall:

- Very shallow in the left tail

- Looks biased high

- Fails KS test

Mack (Paid)

- Overall:

- Slight shallow right tail

- Very shallow left

- Biased high

- Fails KS test

- Two plausible explainations:

- Insurance loss environment has experienced changes

- Other models can validate

Correlated Chain Ladder (Paid) - CCL

- Continue to use “column” correlation

- Add a parameter p to create correlation of losses by AY

- Overall:

- Biased High

- Fails KS test

1Correlated Incremental Trend (Paid) - CIT

- Add “column” correlation - Treat the value at the last diagonal for the row as a random variable

- Add a parameter p to create correlation of losses by AY

- Add CY trend parameter - t

- Applies to incremental losses

- Overall:

- Biased high

- Fails KS test

2 properties of incremental losses

- Skewed right

- Occasionally has negative values

Tighter variance parameters on which 2 variables for the CIT

- t - CY trend

- sigma (d)

Leveled Incremental Trend (Paid) - LIT

- Add “column” correlation - Treat the value at the last diagonal for the row as a random variable

- Add CY trend parameter - t

- Overall:

- Very light left tail

- Biased high

- Fails KS test

Changing Settlement Rate (Paid) - CSR

- Add “column” correlation - Treat the value at the last diagonal for the row as a random variable

- Add parameter “y” that allows for recognition of a speed up in claim payments

- Overall:

- Fits well

- Removed high bias

- No indication of light tails

- Meyers says this is the best model for paid data

Variance (Meyers)

=E(Process Variance) + Var (Hypothetical Means)

=EVPV + VHM

= Process Risk + Paramter Risk (CF)

Larger component of total risk - Parameter or Process Risk

Parameter Risk

Describe three tests for uniformity for n predicted percentiles

Describe two ways to increase the variability of the predictive distribution produced by the Mack model on incurred losses. For each one, identify a model that accomplishes this goal.

Briefly describe two formulations for the skew normal distribution.

- One formulation produces the skew normal distribution by expressing it as a mixed truncated normal-normal distribution

- Another formulation produces the skew normal distribution by expressing it as a mixed lognormal-normal distribution

Briefly describe why model risk can be thought of as a special type of parameter risk.

Model risk is the risk that we did not select the right model. In a sense, we can think of model risk as a special case of parameter risk because the possible models can be thought of as “known unknowns” similar to the rest of the parameters in the model

-

Brosius23

-

Mack (2000)4

-

Mack (1994)17

-

Hurlimann9

-

Shapland & Leong68

-

Venter Factors18

-

Clark18

-

Marshall31

-

Verrall15

-

Meyers28

-

Siewert21

-

Sahasrabuddhe16

-

Teng & Perkins27

-

Patrik14

-

Goldfarb39

-

ERM Ch.114

-

ERM Ch.236

-

ERM Ch.317

-

ERM Ch.422

-

ERM Ch.514

-

Brehm 1 CF Only10

-

Brehm 2 CF Only28

-

Brehm 3 CF Only11

-

Brehm 4 CF Only14

-

Brehm 5 CF Only13