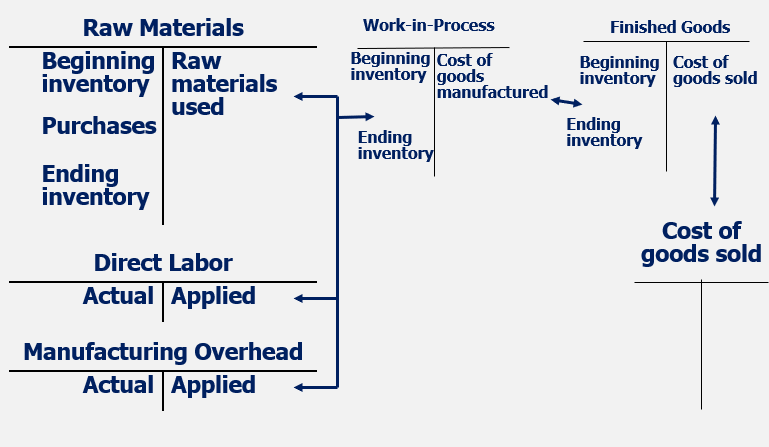

Flow of accounts of the inventory and warehousing cycle:

Notice the connection to the acquisition cycle and payroll cycle

What are the primary business functions involved in the inventory and warehousing cycle?

- Process Purchase Orders

- Receive raw materials

- Store Raw materials

- Process the Goods

- Store Finished Goods

- Ship Finished Goods

7.

Provide a brief description of these business functions involved in the inventory/warehousing cycle:

- Process Purchase Orders

- Receive Raw Materials

Note: these functions part of acquisition cycle as well

Process Purchase Orders

- Acquisition of raw materials/finished goods

- Adequate controls in form of purchase requisitions and purchase orders

Receive Raw Materials

- Goods received, inspected, receiving report made and compared to invoice before payment is disbursed

Provide a brief description of these business functions involved in the inventory/warehousing cycle:

- Store Raw Materials

- Process the Goods

Store Raw Materials

- Material normally placed in warehouse

- Other dept. submits requisition form for disbursement of materials; req form substantiates perpetual invetory

Process the Goods

- Separate production/cost accounting dept. determines cost accounting records

- When jobs completed, costs transferred from WIP to finished goods based on prod. dept reports

What is a perpetual inventory master file?

- File that is updated continuously as raw material moved from storeroom to production or as goods purchased

- Includes info about units acquired, sold, and on-hand and includes unit cost

- In manufactures: Separate master file kept for raw material, WIP, and finished goods

What are the two primary cost systems that exist to transfer costs between inventory accounts?

1) Job Order Costing

- Each job is unique

- Costs of mat./labor accumulated by individual job

2) Process Cost System

- Mass producing the same product

- Costs accumulated per process and unit cost assigned to goods

Provide a brief description of these business functions involved in the inventory/warehousing cycle:

- Store into finished goods

- Ship Finished goods

Store into finished goods

- Once processing complete, product moved to finished goods

- Finished goods perpetual master file added to

Ship Finished goods

- Goods sold to customer

- Shipping document produced and FG master file reduced

What are the 5 parts of the audit of inventory?

- Acquire and record raw materials, labor, and overhead

- Tested in acq./pay and payroll cycle

- Internally Transfer assets and costs

- Ship goods and record revenue and costs

- Tested in sales/collection cycle

- Physically Observe inventory

- Price and compile inventory

The auditor tests internal transfers of assets and costs (part 2 of inventory audit) by:

designing and performing audit tests of cost accounting:

- Test of cost accounting controls

- tests of cost accounting

Cost accounting controls can be divided into two categories:

- Physical controls over raw materials, WIP, and finished goods inventory

- Controls over related costs

How do perpetual inventory master files serve as a cost accounting control?

- Provides record of inventory on hand

- Used to initiate production/acquistion of additional inventory

- Proves record of use of raw materials/sale of finished goods

- Provide record to pinpoint responsibility when differences in inventory counts are discovered

What are the 4 main tests of cost accounting?

- Physical controls over inventory

- Documents and records for transferring inventory

- Perpetual inventory master files

- Unit Costs records

What are some tests for physical control of inventory types?

Generally limited to observation and inquiry

- Inventory protected from theft/misuse

- Locks/assignment of assets

What are the auditor’s primary objectives when observing documents/records for transferring inventory?

What controls tests may be performed?

- Recorded transferes exist (Occurence)

- All transfers recorded (completeness)

- Details of transfer (quant/date) are accurate

Tests:

- Inspect raw materials requisitions for proper approval and compare to perpetual inventory master file

- Compare completed production records with perpetual inventory master file

How can the auditor test the perpetual inventory master files?

What is the importance of testing perpetual inventory master files?

- Examining documentation that supports additions/reductions

- Usually done in the acquisitons/payment cycle (raw materials) and sales cycle (fin. goods)

Importance:

- Affects the timing and extent of physical examination of inventory

- Can be tested throughout period

- when accurate, reduces capacity of inv. count

What is the importance of unit cost records during tests of cost accounting?

What are the tests performed to verify cost records?

Accurate cost data (raw mat/labor/overhead) is essential for fairly stated inventories

Tests:

- Trace units/unit cost of raw materials to master files

- Performed in acq/pay cycle

- Determine and vouch overhead allocation method; usually affected by labor hours

- performed in payroll cycle

Are analytical procedures effective in the inventory cycle?

Yes; can be helpful, though substantive procedures always required

What are some analytical procedures auditors can perform for the inventory cycle?

- What possible misstatements can they indicate?

Compare gross margin % with previous years

Over/understatement of inventory and COGS

Compare inv. turnover (COGS/avg inv) with prev. years

Obsolete inventory ; over/understatement of inv.

Compare manufacturing costs with previous years

Misstatement of unit costs for direct labor/overhead

The most important part of the inventory cycle audit is:

Physical observation of the client’s inventory count and the subsequent testing

Are physical examinations required?

Yes; auditing standards required auditors to satisfy themselves about the effectiveness of client’s representation of quantities and condition

Explain the differences between the client’s and auditor’s requirements for the physical observation of inventory.

Client’s requirements

- Schedule inventory count

- Count 100% of the inventory

- Reconcile differences between files and inventory and make adjustments to master file

Auditor’s requirements

- Understand client’s inventory and protocols

- Evaluating and observing client’s inventory count

- Performing independent tests and counts

- drawing conclusions on adequacy of inventory and client’s policies

What type of test is physical obsevation of inventory?

Dual test: Serves as both an control and substantive test

Control test: Observing client count and ensuring the counting policy/reconciliation works effectively

Substantive test: Auditor’s secondary count substantiates inventory and provides assurance

What key auditing assertions does physical observation address and how?

Key Assetions: Important to test both ways

Completeness: Full testing: Select sample out of items on floor (warehouse) and trace to sheet (inv. records)

Existence: False testing: Select items from sheet (inv. records) and find on floor (warehouse)

Secondary assertions: Cut-off and Realizable value

What controls should be in place and tested during a physical observation of inventory:

- Proper instructions for count

Separation of duties:

- Independent supervisor part of count

- Independent internal verification of counts; 1 employee counts while 1 employee consults record for match

- Reconcilations and adjustments performed by independent employee

-

Module 1 - Review of Audit Theory17

-

Module 2 - Audit of the Sales and Collection Cycle21

-

Module 3 - Audit Sampling23

-

Module 4 - Tests of Details of Balance25

-

Module 5 - Sampling for tests of D.O.B.20

-

Module 6 - Expenses/liabilities of Payment cycle21

-

Module 7 - Acquisitions/Payment Cycle for PPE26

-

Module 8 - Payroll/Personnel Cycle30

-

Module 9 - Inventory/warehousing29

-

Module 10 - Capital Acquisitions/repayment30

-

Module 11 - Cash and Financial Instruments26