What are 2 approaches to model extreme events?

(FERM12)

- Generalized Extreme Value Distribution

- Generalized Pareto Distribution

Describe the general principle behind the Generalized Extreme Value Distribution

(FERM12)

- It considers the maximum observation (Xm) from each sample (of iid RVs), and pools them together to form an extreme loss data population

- As the size of a sample increases, the distribution of the maximum observation converges to the generaized extreme value (GEV) distribution

What is the cummulative distribution function of the GEV?

(FERM12)

What are 2 methods to take extreme values?

(FERM12)

- Return level approach

- Take the highest obervation in each block of data

- Return period approach

- Set a level above which an observation could be regarded as extreme

- Take the observations higher than the level in each block of data

What is a major drawback of the GEV distribution?

(FERM12)

By using only the largest value(s) in each block of data, it ignores a lot of potentially useful information

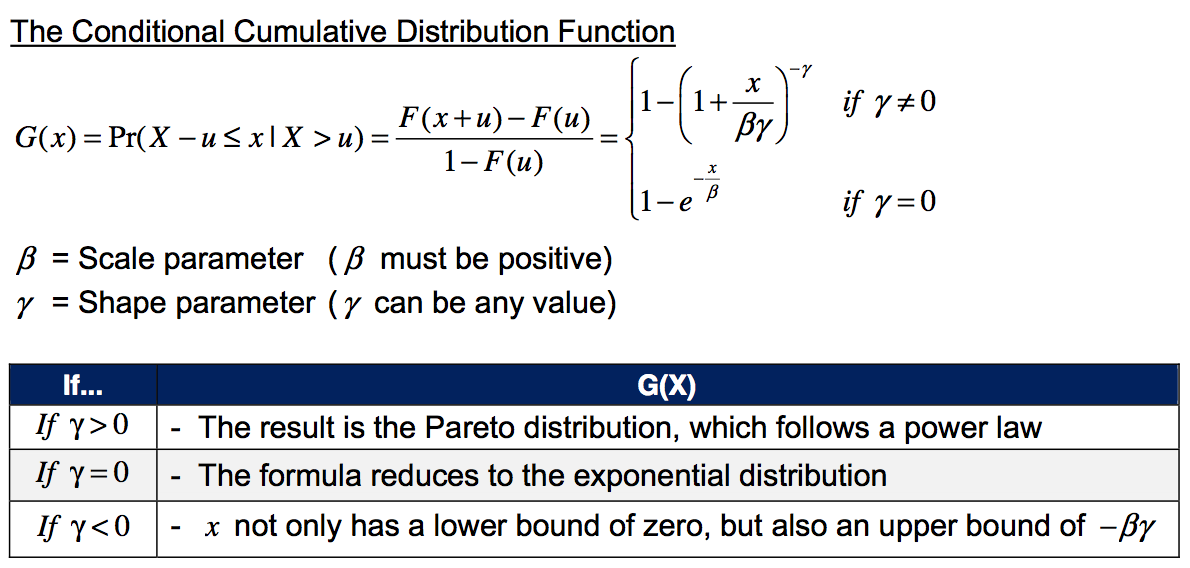

Describe the idea behind the Generalized Pareto Distribution

(FERM12)

- G(x) is the distribution of a RV X in excess of a fixed hurdle u given that X is greater than u

- Assume the observations are iid

- As the threhold increases, the distribution of the conditional loss distribution converges to a GPD

What is the cummulative distribution of GPD?

(FERM12)

What is a key consideration when using GPD?

(FERM12)

Choosing the right omega threshold

What are 3 characteristics of financial time series?

(FERM14)

- Serial correlation does not exist to the extent that it is possible to make money from it

- There is strong serial correlation in a series of absolute or squared returns

- The distribution of market returns appears to be leptokurtic (i.e., extreme values tend to occur closely together)

What are 3 characteristics of multivariate return series?

(FERM14)

- Correlations do exist between stocks, and between asset classes and economic variables

- There is little evidence of cross-relation (i.e., change in stock price t has little effect on stock price t+1)

- The time series of extreme returns are individually leptokurtic and they have jointly fat tails

What are the 3 most common ways to measure spread?

(FERM14)

- Nominal Spread

- Static Spread

- Option-Adjusted Spread

What is nominal spread and how is it calculated?

(FERM14)

- The difference between the gross redemption yields of the credit security and the reference bond (e.g., a treasury bond)

- Quick and easy to measure/calculate

NS = rGY - rREF

What is static spread and how is it measured?

(FERM14)

- The addition to the risk-free rate required to value cash flows at the market price of a bond

- It considers the full risk-free term structure and the constant (spread) SC added to the yield at each duration

Bond Price = Sum over t [CashFlowt / (1 + rf,t + SC)]

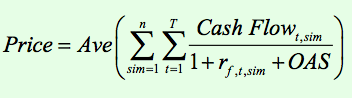

What is the option adjusted spread and how is it applied to calculate Bond Price?

(FERM14)

- Allows for a large number of stochastically generated interest rates (rf,t,sim) such that the expected yield curve is consistent with that seen in the market

- It considers any options that are present in the credit security (OAS)

How are government bonds’ expected returns estimated?

Both domestic and overseas government bonds are risk-free

Returns are estimated from the gross redemption yield, an annual compound interest rate

What is the difference between corporate bonds and government bonds?

What is credit spread?

(FERM14)

- Corporate bonds are not risk-free and have a chance of default, so their expected returns should consider a risk premium

- Credit spread represents the additional return offered to investors with repect to the credit risk being taken

What are 5 reasons why the credit spreads are higher than historical studies’ findings?

(FERM14)

- Credit risk premium - reward for volatility relative to risk free securities

- Liquidity risk premium - reward for lower liquidity compared to government bonds

- Risk aversion premium - reward for possibility of extreme events and skeyness of bond payoff structure

- Tax premium - less favorable treatment compared to government

- Correlation premium - correlation between credit spreads and interest rates is typically negative

What CAPM and what is the formula behind it?

(FERM14)

Capital Asset Pricing Model

rx = r* + ßx (ru - r*) where

rx = rate of return on individual investment X

r* = risk-free rate of return

ru = market return

ßx = σxpx,u / σu

What are the 6 properties of a good benchmark?

(A good benchmark is important when considering market risk!)

(FERM14)

- Unambiguous (components and constituents should be well-defined)

- Investable (can buy components of a benchmark and track it)

- Measurable (can quantify the vaue of a benchmark with reasonable frequency)

- Appropriate (consistent with investor’s style and objectives)

- Reflective of current investment opinion (contains components about which investor has opinions)

- Specified in advance (known by all participants before the period of assesment)

What is are 8 specific criteria against which a benchmark can be measured in its appropriateness?

(A good benchmark is important when considering market risk!)

(FERM14)

- Proportion (should contain a high proportion of the securities held in the portfolio)

- Turnover (benchmark’s constituents’ turnover should be low)

- Allocations (shoud be investable position sized)

- Position (investor’s active position should be given relative to the benchmark)

- Variability (benchmark variability to the portfolio should be lower than market variability to portfolio)

- Positive correlation between rX - rU and rB -rU

- Zero correlation between rX - r<span>B</span> and rB -rU

- Style exposure (must be similar between portfolio an benchmark)

What is the Black-Scholes Model used for?

What are the formulas?

(FERM14)

Used to model European call and put options

Call = C0 = X0 N(d1) - Ke-r*T N(d2)

Put = P0 = Ke-r*t N(-d2) - X0 N(-d1)

where

d1 = [ln(X0/K) + (r* + σ2X/2)T] / [σX sqrt(T)]

d2 = d1 - σX sqrt(T)

What are two types of interest rates?

(FERM14)

- Spot rates

- (1 + rt)-1 = e-st

- Forward rates

- e-st = e -(f1 + f2 + … + fT)

What is the bootstrapping approach?

(FERM14)

Constructing a spot rate curve from the gross redemption yields on a series of bonds with a range of terms

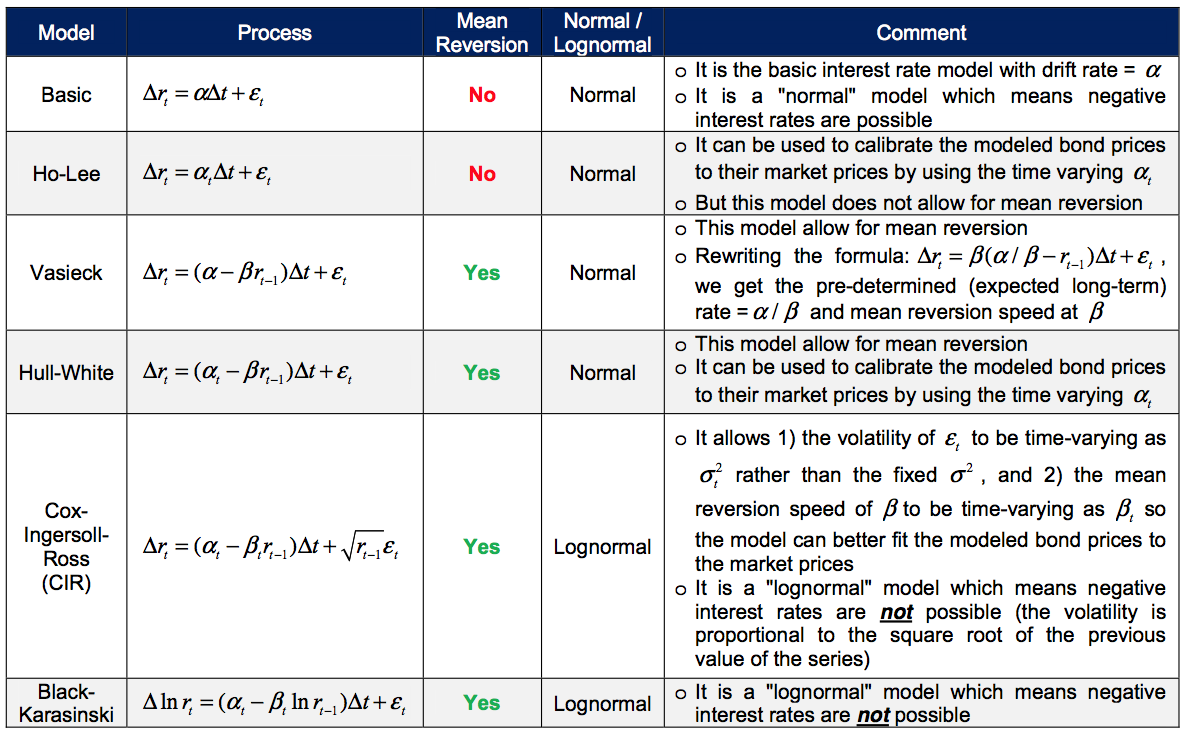

What are 6 single-factor interest rate models?

(FERM14)