What is Auditing ?

is the accumulation and evaluation of evidence about information to determine and report on the degree of correspondence between the information and established criteria. Auditing should be done by a competent, independent person.

What is the purpose of Auditing

The purpose of an audit is to provide financial statement users with an opinion by the auditor on whether the financial statements are presented fairly, in all material aspects, in accordance with the applicable financial accounting framework. An auditor’s opinion enhances the degree of confidence that intended users can place in the financial statements.

Accounting vs. Auditing

Accouting:

- Proper recording, classifying and summarizing of economic events on a timely basis and at a reasonable cost

- Goal: Provide financial information for decision making

Auditing:

- Determine whether recorded information properly reflects the economic events that occurred during the accounting period

- Goal:Accumulation and interpretation of audit evidence

The Role of Auditing in Corporate Governance

Asymmetric information

- An aspect of an interaction is unknown or not observable by one party of the interaction

- Typically:

- Important characteristics for the interaction are not observable before the contract is signed (adverse selection)

- Counteracting through sending specific signals (signalling)

- Important characteristics for the interaction are not observable after the contract is signed (moral hazard)

- Counteracting through profit sharing

- Creation of win-win situations

Principal agent theory

- Principal = Owner, Agent = Management

- Principals mandate agents to lead and manage the company -

- Principals and agents may have diverging goals and interests, both may try to maximize their personal gain and utility

- Strategies have to be developed that allow the coordination of these different objectives through effective control systems

Why Do We Need Auditing? -> Managing the Principal Agent Problem

From an agency perspective, auditing:

- is regarded as a cost-effective monitoring device

- reduces information asymmetries by adding credibility to financial statements

- has an important role in a setting where ownership and management of the firm is separated and in the relationship between managers and creditors

- reduces risk for investors

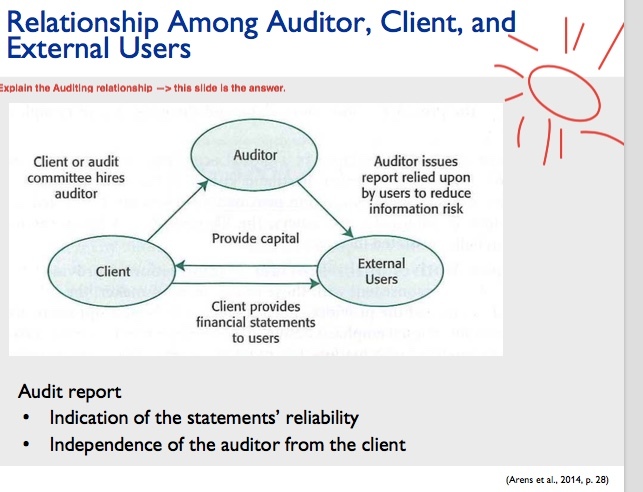

Relationship Among Auditor, Client, and External Users

Non-Transferable Duties of the Board of Directors

Art. 716a para. 1-2 Swiss Code of Obligations (CO)

A).The board of directors has the following non-transferable and inalienable duties:

(1) the overall management of the company and the issuing of all necessary directives;

(2) determination of the company’s organization;

(3) the organization of the accounting, financial control and financial planning systems as required for management of the company;

(4) the appointment and dismissal of persons entrusted with managing and representing the company;

(5) overall supervision of the persons entrusted with managing the company, in particular with regard to compliance with the law, articles of association, operational regulations and directives;

(6) compilation of the annual report, preparation for the general meeting and implementation of its resolutions;

(7) notification of the court in the event that the company is overindebted.

B) The board of directors may assign responsibility for preparing and implementing its resolutions or monitoring transactions to committees or individual members. It must ensure appropriate reporting to its members.

Responsibility of the Management

- Preparation of financial statements in accordance with applicable accounting frameworks

- Integrity and fairness of the representations (assertions) in the financial statements: presentations and disclosures

- Certification of the financial statements submitted to the SEC

− Financial statements fully comply with the requirements

− Information are fairly presented, in all material respects

- Internal Control

− Establishing and maintaining internal controls that provide reasonable, but not absolute, assurance that the financial statements are fairly stated

− Publicly report on the operating effectiveness of controls

Responsibility of the Auditor

- Expression of an opinion based on the evaluation of the annual report

- Plan and execute the audit in the manner, that material misstatements can be detected with reasonable assurance

- Conduct audit with adequate skepticism

- Errors or fraud may lead to material misstatements; hereby one differentiates between

- Error: unintentional misstatement of the financial statements, not criminally relevant misstatements or omissions

- Fraud: intentional, criminally relevant acts or omissions, committed by members of the management, employees or third parties

- Internal Control

- Obtain understanding of internal control

- Express an opinion on controls

Rules of Conduct

1) Independence

– Assurance in dependence

– Independence of mind/infact

– Independence in appearance

2) Integrity and Objectivity

3) Confidentiality

4) Professional competence and due care

Assurance Independence

“Assurance independence is an absence of interests that create an unacceptable risk of material bias with respect to the quality or context of information that is the subject of an assurance management.” (AICPA)

- Material bias: a reasonable person with knowledge of the assurer’s interests in the information or context would conclude that the assurer’s objectivity is impaired

- Information: includes the output of information systems that are the subject of assurance engagements

Assurance independence refers only to the absence of interests that can create material bias in the sense of partisan judgment

Independence of Mind/in Fact

A) Auditor’s state of mind that permits the audit to be performed with an unbiased attitude: unbiased forming of an opinion

B) Ability to resist certain pressures

C) Determinants for independence of mind:

– Professional ethics for auditors

– Personality and character of the auditor which are formed by his education and professional experience

Summary Independence of Mind

The state of mind that permits the provision of an opinion without being affected by influences that compromise professional judgement, allowing an individual to act with integrity, and exercise objectivity and professional skepticism.

Independence in Appearance

- Result of other’s interpretations of independence of mind/fact

- Value of auditing depends on the public’s perception of the independence of auditors

- Achieved through avoidance of facts and circumstances which are essential in the manner that a third party may doubt the auditor’s objectivity

- Linked to several direct and indirect factors but it is not regulated by law

Summary Independence in Appearance

The avoidance of facts and circumstances that are so significant that a reasonable and informed third party, having knowledge of all relevant information, including safeguards applied, would reasonably conclude a firm’s, or a member of the assurance team’s, integrity, objectivity or professional skepticism had been compromised.

Independence According to International Federation of Accountants (IFAC)

a. Financial independence

b. Irreconcilable activities (membership in the management board, employment)

c. Family or other personal ties

d. Concentration risk regarding salary

e. Performance-based remuneration

f. Acceptance of gifts or services

g. Involvement in the same lawsuits

h. Long-term auditor-client relationships

Integrity and Objectivity

- In the performance of any professional service, a member…

…shall be free of conflicts of interest

…shall not knowingly misrepresent facts

…shall not subordinate his or her judgement to others, e.g., supervisors on the audit

- Freedom from conflicts of interest:

Absence of relationships that might interfere with objectivity of integrity

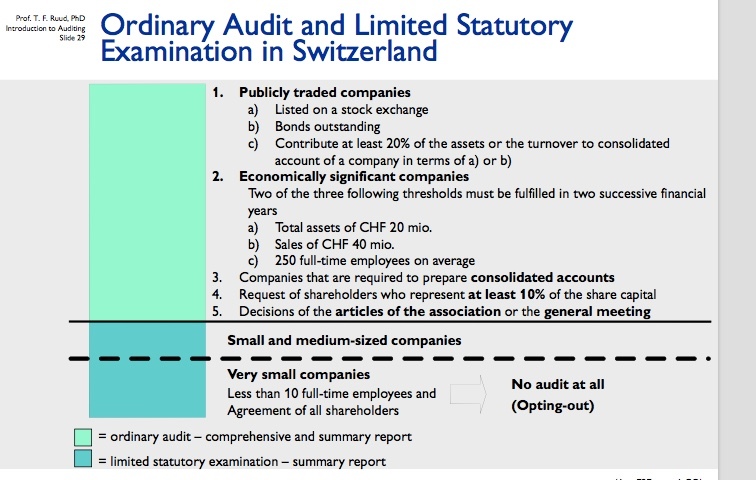

Ordinary Audit and Limited Statutory Examination in Switzerland

- Publicly traded companies a) Listed on a stock exchange b) Bonds outstanding c) Contribute at least 20% of the assets or the turnover to consolidated account of a company in terms of a) or b) 2. Economically significant companies Two of the three following thresholds must be fulfilled in two successive financial years a) Total assets of CHF 20 mio. b) Sales of CHF 40 mio. c) 250 full-time employees on average 3. Companies that are required to prepare consolidated accounts 4. Request of shareholders who represent at least 10% of the share capital 5. Decisions of the articles of the association or the general meeting –> ordinary audit – comprehensive and summary report ——————————————————————————– Small and medium-sized companies Very small companies Less than 10 full-time employees and Agreement of all shareholders –> No audit at all (Opting-out)

Factors Significantly Associated with Demand for Voluntary Audit (Private Firm Research)

Separation between ownership and control

Relationship to lender / high gearing ratio

Firm size (turnover)

Management’s perception of audit quality

Use of external accountant

Purchase of nonaudit services from audit firm

Independence According to the Swiss Code of Obligations (I/III)

- Due to the distinction between the ordinary audit and the limited statutory examination, requirements for independence are regulated differently according to the type of audit

- Art. 728 para. 1 CO and Art. 729 para. 1 CO rule:

“The auditor must be independent and form its audit opinion objectively. Its true or apparent independence must not be adversely affected.”

Independence According to the Swiss Code of Obligations

(II/III) Independence at the ordinary audit (Art. 728 para. 2 CO)

The following are in particular not compatible with independence:

- Membership of the board of directors, any other decision-making function in the company or any employment relationship with it

- A direct or significant indirect participation in the share capital or a substantial claim against or debt due to the company

- A close relationship between the person managing the audit and a member of the board of directors, another person in a decision-making function, or a major shareholder

- The involvement in the accounting or the provision of any other services which give rise to a risk that the auditor will have to review its own work

- The assumption of a duty that leads to economic dependence

- The conclusion of a contract on non-market conditions or of a contract that establishes an interest on the part of the auditor in the result of the audit

- The acceptance of valuable gifts or of special privileges

Independence According to the Swiss Code of Obligations (III/III)

Independence at the limited statutory examination (Art. 729 para. 2 CO)

- Involvement in the accounting and the provision of other services for the company being audited are permitted.

- In the event that the risk of auditing its own work arises, a reliable audit must be ensured by means of suitable organizational and staffing measures.

Objective of Conducting an Audit of Financial Statements

The purpose of an audit is to provide financial statement users with an opinion by the auditor on whether the financial statements are presented fairly, in all material respects, in accordance with the applicable financial accounting framework. An auditor’s opinion enhances the degree of confidence that intended users can place in the financial statements

Steps for the Development of Audit Objectives

- Financial statements are divided into smaller segments

- Each segment is audited separately but not on a completely independent basis

- After the audit of each segment is completed: combine results and conclude about the financial statements taken as a whole

- Cycle approach

– Idea: keep closely related types or classes of transactions and account balances in the same segment

– Makes the audit more manageable

– Considers the risk and the materiality within each field

– Aids in the assignment of tasks to different members of the audit team

Determination of Audit Objectives: Transaction-Related and Balance-Related

Transaction-related audit objectives

– Closely related to management’s assertions about classes of transactions

– Framework to help the auditor accumulate sufficient appropriate evidence related to classes of transactions, e.g., purchase of inventory

– General transaction-related audit objectives vs. specific transaction- related audit objectives

Balance-related audit objectives

– Closely related to management’s assertions about account balances

– Framework to help the auditor accumulate sufficient appropriate evidence related to the ending balance in balance sheet accounts, e.g., inventory

– General balance-related audit objectives vs. specific balance-related audit objectives

integrity and objectivity means

- In the performance of any professional service, a member…

…shall be free of conflicts of interest

…shall not knowingly misrepresent facts

…shall not subordinate his or her judgement to others, e.g., supervisors on the audit

- Freedom from conflicts of interest:

Absence of relationships that might interfere with objectivity of integrity