In deciding the cost of inventory….

- What is absorption costing (full costing)?

- What is marginal costing?

- A method of building up a full product cost which adds direct cost and a proportion of production overheads.

- Prime costs (direct costs) + variable costs only (no fixed costs)

Define the standard cost

What is the fair share of fixed production costs?

Absorption costs = marginal costs + fair share of fixed production costs.

Essentially fixed production overheads

What are the 3 steps to absorbing fixed prouction overheads into costs per unit.

- Alloction and appportionment of overheads to all production cost centres.

- Re-apportioning of overheads that do not produce inventory.

- Absorbing overheads into units of inventory

Step 1. Alloction and appportionment of overheads to all production cost centres.

- How are overheads that arise in 1 department allocated

- How are overheads relating to a whole factory allocated?

- They are allocated to that departments cost centre.

- They are apportioned on a fair basis. e.g. factory rent may be apportioned in relation to the floor area occupied by each department or cost centre.

What does it mean to ‘apply factory wide’ or at a ‘blanket rate’?

When overheads should be apportioned but a company has simply divided total overheads for the factory by the number of units

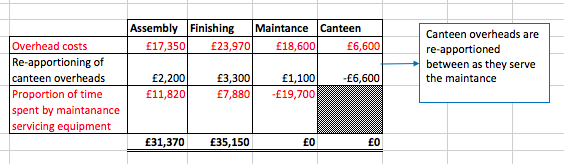

Step 2: Re-apportioning of overheads that do not produce inventory.

What does this involve?

Re-apportioning the cost from departments that don’t produce inventory (often services) to the inventory producing departments

What should be done if there is more than one service centre for which costs need to be reappointed.

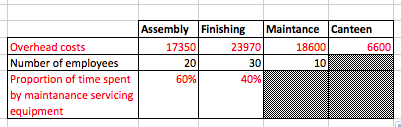

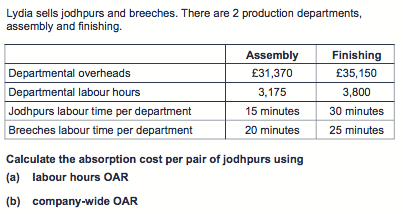

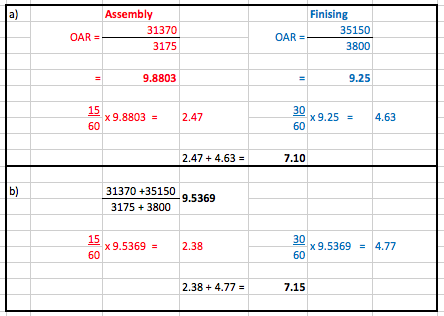

Bellow are the overhead costs for each department. Only Assembly and Finishing produce inentory.

Re-apportion overheads using the infomation provided.

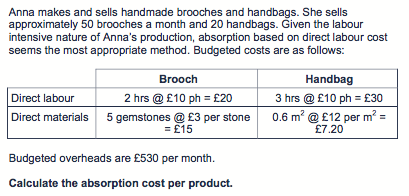

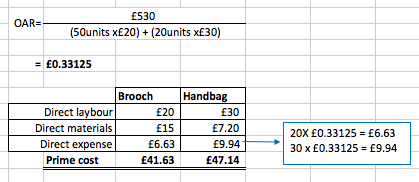

Step 3: Absorbing overheads into units of inventory

- What does this do?

- How is this calculated?

- Give example of budgeted activity

- Assigns the costs caluclated in step 1 and 2 to 1 unit of inventory.

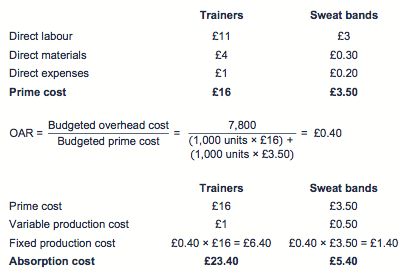

- Using an overhead absorption rate = Budget ed overhead cost (calculated in step 1 & 2) / Budgeted activity

- Number of units, Prime costs, Direct laybour/machine costs, & Direct laybour/machine hours.

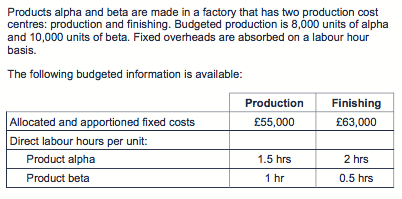

What is the budget fixed cost per unit for alpha and beta?

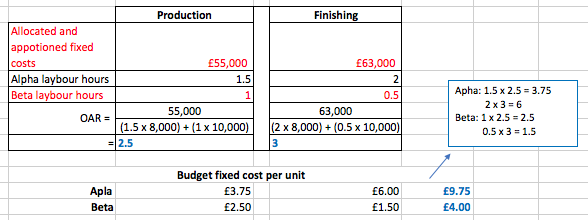

At the end of the year how do you calculate over or under absorption?

- What are balanket absorbtion rates <em>(single factory rates)</em>?

- When are they appropriate to use?

- A single absorption rate is used for ll cost units irrisepctiv of departments.

- When an individual departments OARs are likely to be similar to that of the whole company.

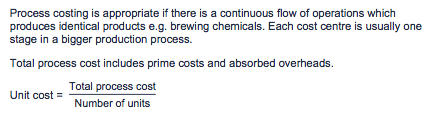

- What does process costing involve and when is it appropriate.

- What is life style costing?

- What is target costing?

What is ‘Just in time’ production?

Producing goods or services when required by the customer → therfore no inventory is held.

- What does job costing involve and when is it appropriate.

- Contract costing?

- Batch costing?

- Prime costs and absorbed overheads → appropriate for specific one-off jobs of a short duration.

- Prime costs, allocated oevrheads & absorbed overheads • appropriate for one off long duration jobs.

- Prime costs and absorbed overheads → appropriate for a group of identical cost unit jobs.

-

Chapter 117

-

Chapter 29

-

Chapter 320

-

Chapter 412

-

Chapter 512

-

Chapter 6 - budgeting11

-

Chapter 6 - forecasting10

-

Chapter 7 - Working capital14

-

Exam questions13

-

Chapter 89

-

Chapter 913

-

Chapter 10 - break even analysis.14

-

Chapter 11 - Investment appraisal - non discounting12

-

Chapter 11 - Investment appraisal - discounting20

-

Chapter 1 - 8 pre exam questions21