Properties of Σt

- is spd k-by-k matrix

- has k(k+1)/2 “free parameters”

Challenges of multivariate modeling

- Curse of dimensionality

- Cost of evaluating the likelihood

- Ensuring well-defined dynamics

Aims of multivariate covariance modeling

- Parameterising the dynamics cheaply

- Keeping the dynamics of the model realistic

Alternative parameterisation of Σt

DtRtDt

Where: D is a diagonal matrix that contains the conditional standard deviations (k free parameters)

R is a conditional correlation matrix (k(k-1)/2 free parameters)

Does the correlation matrix change over time?

Yes.

A curse upon it.

VEC/BEKK models

- Generalisations of GARCH models for multivariate data

- Flexible but impractical for large numbers of coefficients

VEC(1,1)

ht = c + Ant-1 + Ght-1

ht = vech(Σt)

nt = vech(rtrt’)

VEC(1,1)

Number of parameters to estimate

k (k+1) (k( k+1) +1)/2

Like basically shitloads.

DVEC

Is a VEC model where the matrices A and G must be diagonal

Has “only” k(k+5)/2 parameters

In case of the DVEC model, conditions to ensure that the conditional covariance is positive definite are typically derived by

expressing the model in terms of Hadamard products

the BEKK model was introduced to

make it easier to estimate Σt in such a way that it remained psd

The BEKK model

Σt = C’C + A(rt−1rt−1‘)A + GΣt−1G

Drawback of BEKK parameterisation

Coefficients are harder to interpret

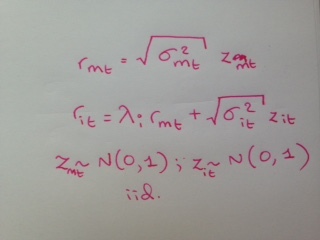

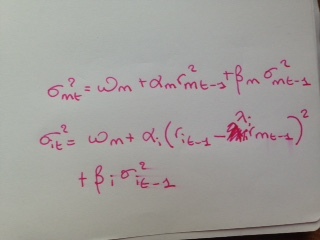

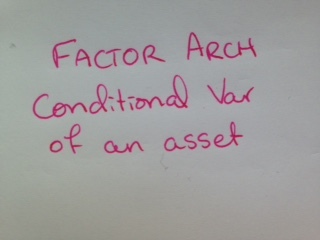

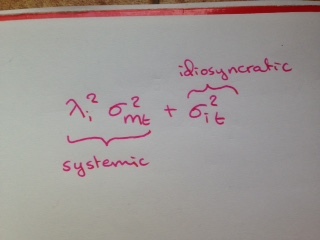

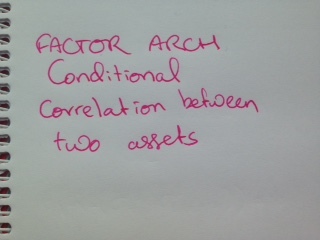

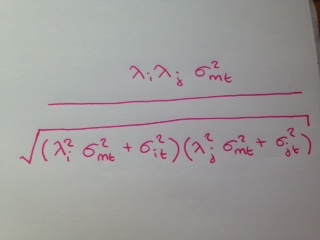

Pros of factor ARCH model

- easy to interpret

- consistent with financial theory

- number of parameters increases linearly with number of assets

- Estimation can be decomposed in a series of univariate estimations

Cons of factor ARCH model

- Conditionally on market, returns are independent

- Factor loading coefficient is not allowed to change over time