1

Q

A

2

Q

A

3

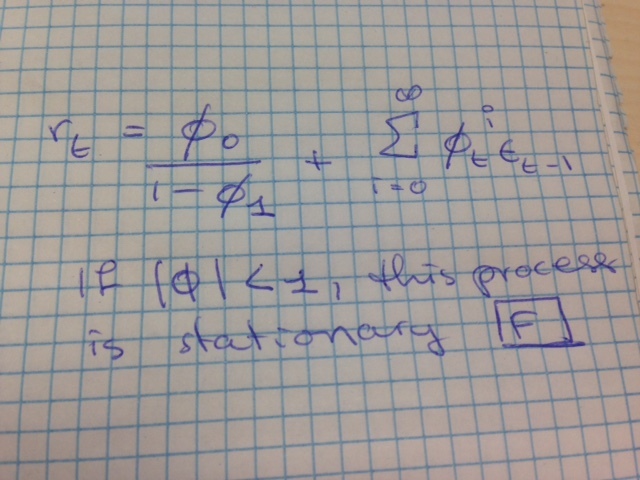

Q

rt is weakly stationary if

A

4

Q

A

5

Q

A

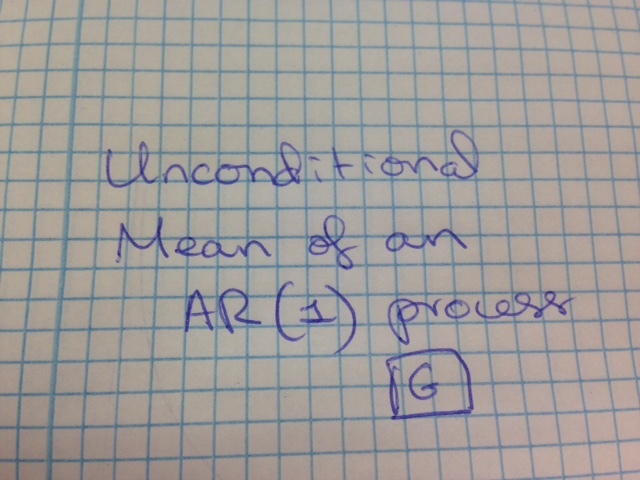

6

Q

AR(1)

For all lags greater than 1, the partial autocorrelation…

A

is 0

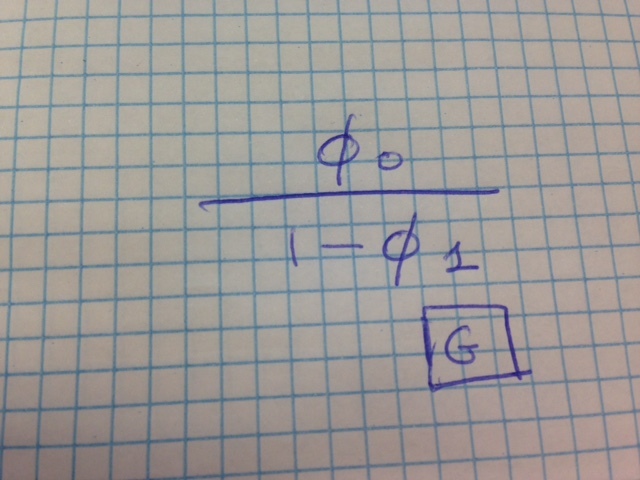

7

Q

A

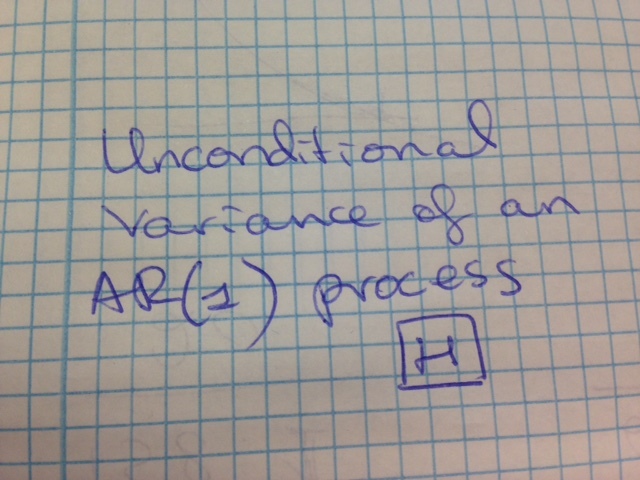

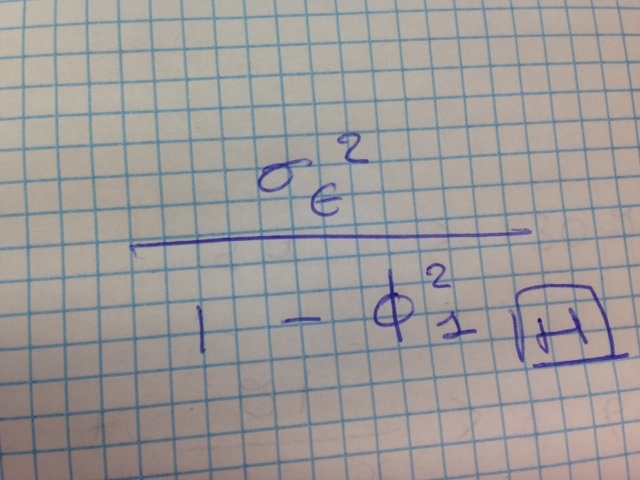

8

Q

A

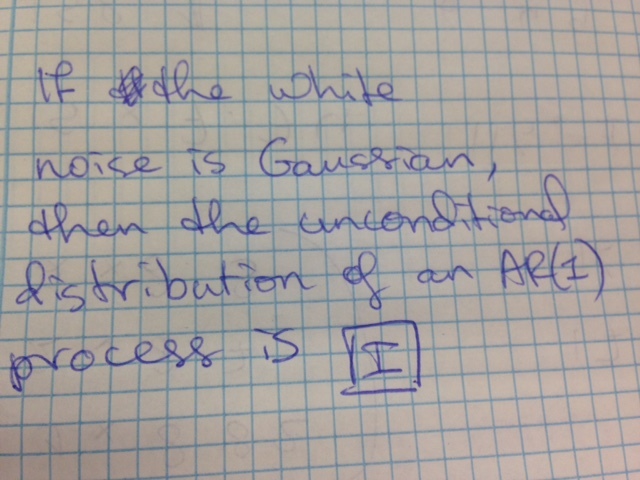

9

Q

A

10

Q

A

11

Q

A

12

Q

A

13

Q

A

14

Q

A

15

Q

AR(1)

Lag k partial auto-correlation

A

0

16

Q

An MA(1) is said to be invertible when

A

It can be represented as an autoregressive model with infinite lags

17

Q

Unconditional mean of an MA(1)

E(rt) =

A

c0

18

Q

MA (1)

Model

A

19

Q

A

20

Q

A

21

Q

A

22

Q

A

23

Q

A

24

Q

A

25

26

27

28

29

30

31

32

33

34

35

Financial Econometrics

flashcards

Decks in class (10)

# Cards