Non-Community Property Interest

- Income earned by spouses prior to marriage

- Property received as a gift by one spouse

- Property inherited by one spouse

- Interest earned on separate assets held by one spouse as a sole owner

Community Property

- With assets held as CP each spouse owns a separate, undivided, equal interest in the property

- All property ecquired by spouses during marriage are presumed to be CP

- Property gets FULL step-up in basis (only LTCG property), if at least ½ of the whole property is includible in deceased spouse’s gross estate

- Note: Property enjoys a 100% step-up in basis, but only ½ is included for estate tax pruposes*

- ** watch out for Section 121 Exemption real property questions*

Joint Tenancy with Rights of Survivorship (JTWROS)

- Property can be held by husband and wife, parent and child or children, siblings, and business partners

- Control, ownership, and enjoyment shared equally by all joint tenants

- Upon death of each tenant, property immediately passes to surviving joint tenants in equal shares.

- Property NOT controlled by terms of the will

- NOT subject to probate

Tenancy by the Entirety

- Ownership can only be held by a husband and wife

- Transfer of property can only occur with the mutual consent of both parties

- In most states, property is protected from the claims of each spouse’s separate creditors, but NOT protected from the claims of both spouse’s joint creditors

Tenancy in Common

- Two or more owners each own an undivided interest in the property

- Any Income is distributed according to each owner’s respective share in the property

- Owners are free to transfer their respective share of the property to other individuals

- Ownership stake goes through probate upon death

Assets NOT Subject to Probate

(Will Substitute)

- JTWROS

- TBE

- TOD/POD

- Totten Trust

- Transfer by contract: Named beneficiaries for qualified/retirement plans, IRAs, Life insurance and annuities

- Deeds of title

- Trust: Revocable and/or Irrevocable

Assets Subject to Probate

- “Singly” owned assets

- Property held by Tenancy in Common (TIC)

- Assets where the beneficiary is the “Estate of the Insured”

- Community Property (CP)

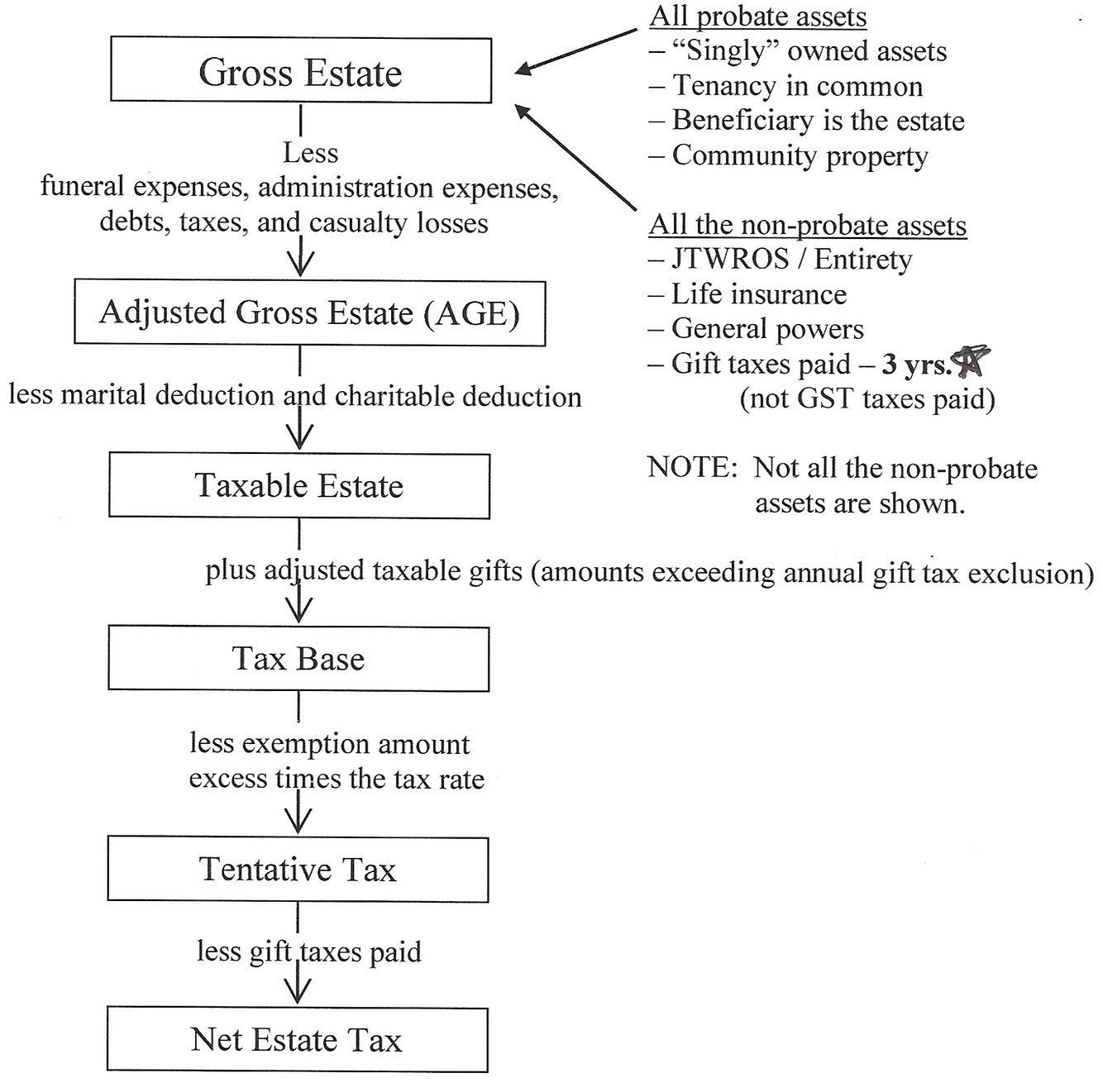

Form 706

Assets Included in the Gross Estate

- Singly Owned Assets

- Tenancy in Common

- Beneficiary is the Estate

- Community Property

- JTWROS/Entirety

- Life Insurance

- General Powers

- 3-year gross-up on gift taxes paid (but NOT GST taxes paid)

Incidents of ownership

(definition and inclusions)

the right to:

- change beneficiaries

- assign

- terminate

- borrow against the cash reserves

- name beneficiaries (if you reassign and don’t change bene)

- hint: CATBN

*Premium paying is not an incident of ownership

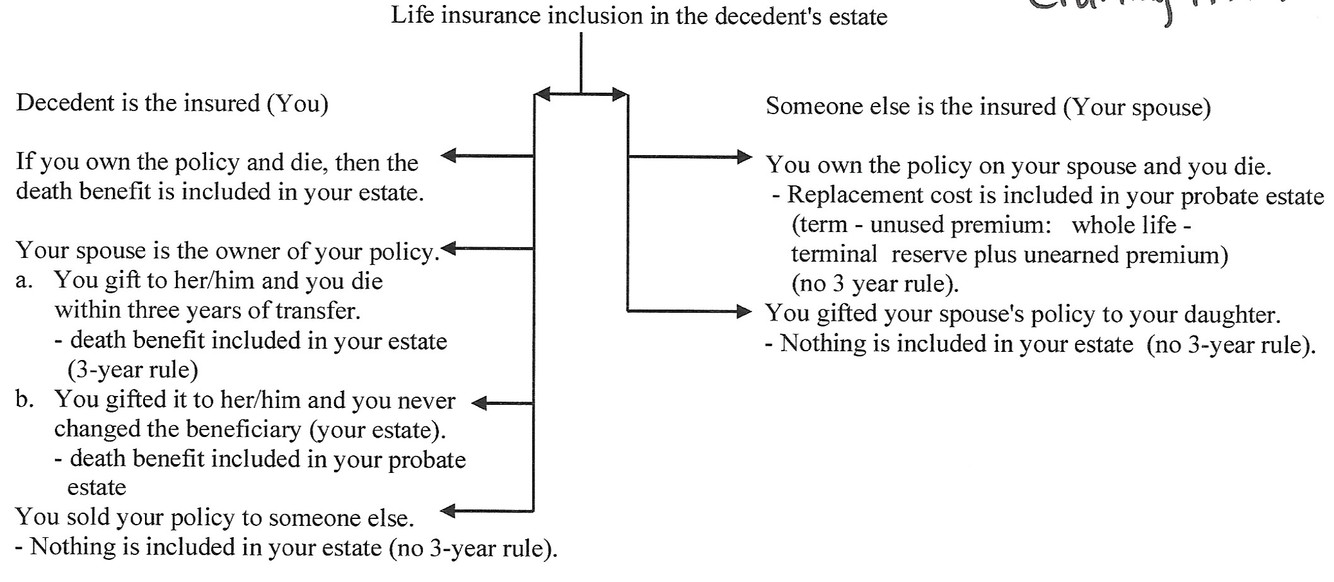

Life Insurance Added to the Estate

- Proceeds are paid to the Executor of the Decedent’s Estate

- Decedent at Death possesses an Incident of Ownership in the policy

- Decedent transferred a policy with an Incident of Ownership within 3 years of death

Valuation of a Gift

The value of a gift for gift tax purposes is its fair market value (FMV) at the date of gift.

Present Interest Gift Vehicles

- UGMA/UTMA

- 2503(c) Trust

- Section 529 College Savings Plan

- Crummey Trust

*Present interest gifts qualify for the $15,000 annual exclusions

Future Interest Gift Vehicles

- 2503(b) trust

- remainder interest

- a trust in which income will be accumulated for a period of years

*gift of a future interst doesn’t qualify for the $15,000 annual exclusion

Basis of a Gift

- If FMV on the date of gift is greater than the donor’s Adjusted Basis, use the donor’s Adjusted Basis.

- If FMV of the gift is less than the donor’s basis, use the chart below:

Client’s Subtituted Basis/Dual/Double Basis

- Above Substitute Basis = Gain

- Between Basis and FMV = NO Gain or Loss

- Below FMV = Loss

Deductible Gifts (Not Taxable Gifts)

Also called Exempt Gifts or Qualified Transfer

- Gifts to a spouse, provided they are not a Terminal Interest

- Gifts to qualified charities

- Qualified payment in any amount made directly to an educational institution for tuition

- Qualified payment in any amount made directly to a medical care provider on behalf of any individual

- Gifts to American political parties

Summary of Rules Regarding Gifts and the Donor’s Estate

- Generally, gifts given are simply “Taxable Gifts” to the extent such gifts exceed the Annual Exclusion.

- Taxable Gifts are added to the Taxable Estate

- Gift Taxes paid (or payable) are generally allowed as credit against the Tentative Tax

- Gift Taxes paid on any gifts within three years of death are added to the Gross Estate

Powers of Attorney

- Traditional, Non-Durable Power of Attorney: Power ceases when the principal is no longer legally competent

- Durable Power of Attorney: Authority of agent continues when principal become incompetent

- Springing Durable Power of Attorney: Main strength is the agent has no authority over the principal’s assets until incompetency.

Power of Appointment (Trusts)

- General Power: Holder may exercise the power in any manner he/she wishes

- Ascertainable Standard: Relating to health, education, maintenance, or support (HEMS)

- Special Power: Exercisable only with the consent of the creator of the power or a person having a Substantial Adverse Interest

Hint: GAS

Gift and Estate Tax Implications (General Power)

- Gift Tax Implications (General Power)

- Exercised, Released, or Lapsed → Taxed

- Lapsed with a “5 or 5” power →Not Taxed

- Estate Tax Implications (General Power)

- Exercised, Released, or lapsed →Taxed

- Exercised, Released, or Lapsed with a “5 or 5” power → Greater of the “5 or 5” is taxed

“5 or 5” Power

Property subject to a General Power will be included in a donee decedent’s Estate (or considered a “Taxable Gift”) only to the extent that the property exceeds the greater of:

- $5,000, or

- 5% of the total value of the fund subject to the power as measured at the Time of Lapse

- Not exercised → 5 of 5 is included in estate*

- Exercise & spend → nothing is included*

- Exercise & save → nothing from trust is included, but unspent funds are*

Grantor Trust Rules (Tainted / Defective Trusts)

Income Tax & Estate

- Trust may be Defective / Tainted for Income Tax and Estate Tax purposes if the Grantor retains:

- A Right to Income or the Right to Use/Enjoy Trust property (Beneficial Enjoyment)

- A Reversionary Interest exceeding 5% (Retained Interest)

Elements of a Trust

- In order for a Trust to exist, there must be Property (also known as Principal, RE, or Corpus)

- There must be a Grantor. This is any person who transfers Property to and dictates the terms of a Trust.

- There must be a Trustee who received legal title to the Property placed in the Trust, and who generally manages and distributes income according to the terms of a formal written agreement (Trust Instrument).

- There must be a Beneficiary who has Equitable Title to the property.

- The Grantor and Trustee must be legally competent.

Simple

vs.

Complex Trusts

Simple Trusts (2503(b), Marital, QTIP) are considered merely a “conduit” for forwarding income to the Beneficiaries (Pass-Through)

Complex Trusts (2503(c)), are separate Tax Entities and taxed as such if it meets two requirements:

- It is irrevocable, and the Grantor has not retained any control

- Income is accumulated