Clark: What are the primary objectives of Clark’s paper? What are the two key elements from those objectives?

Objective 1:

- to provide a tool that describes the loss emergence

Objective 2:

- to provide a way of estimating a range of possible outcomes around the expected reserve

The 2 key elements:

- the expected amount of loss to emerge in some time period

- the distribution of actual emergence around the expected value (stochastic reserving)

Clark: Expected Loss Emergence

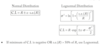

Weibull

- generally provide small tail factor than Loglogistic

- if given Wiebull on the exam, you shouldn’t need to truncate the data or need a tail factor

- Loglogistic you will require to truncate as it has a heavier tail

- note that ‘x’ is cumulative time average so from accident year to valuation point and then half of the last valuation point (so 120 months then ‘x’ is 114)

Clark: Expected Loss Emergence

Loglogistic (Inverse Power)

Clark: What are the advantages of using parameterized curves to determine the expected emergence pattern?

- simple method as we only need to estimate 2 parameters

- can use triangles with partial periods

- indicated pattern is a smooth pattern and will not have random movement seen in the historical age-to-age factors

Clark: What is the benefit of using the Loglogistic and the Weibull curves to derive the reporting pattern?

- Smoothly move from 0% to 100%

- these two models will work when some actual points show decreasing losses; however, if there is real expected negative development then a different model should be used

- e.g. significant salvage recoveries you may see on physical damage

- these two models will work when some actual points show decreasing losses; however, if there is real expected negative development then a different model should be used

- Closely match empirical data

- First and second derivatives are calculable

- Can be used on partial periods

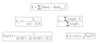

Clark: Estimating Ultimate Losses

LDF Method

µAY;x,y = ULTAY * [G(y|w,ø) - G(x|w,ø)]

Clark: Estimating Ultimate Losses

Cape Cod Method

Explain why CC is better than LDF method?

µAY;x,y = PremiumAY * ELR * [G(y|w,ø) - G(x|w,ø)]

- Cape Cod method has a smaller parameter variance

- Process variance can be higher or lower than the LDF method

- In general, Cape Cod is preferred to LDF method since:

- LDF method is overparameterized due to less data points as we are using annual triangle

- CC has lower total variance driven by

- reduced number of parameters

- using more information (premium/exposure base)

Clark: The distribution of actual loss emergence process variance is given by the following:

σ2 = ?

- assume that c follows an over-dispersed Poisson distribution with scaling factor σ2

- this is the same thing as the Chi-Square error term which is then scaled by n-p

Clark: What are the advantages of using the over-dispersed Poisson distribution?

Advantages

- scaling factors allow us to match the first and second moments of any distribution which offers a high degree of flexibility

- MLE produces the LDF and CC estimates of ultimate losses so can be presented in format familiar to reserving actuaries

Clark: Should we be concerned about estimating ultimate reserves using a discrete (Poisson) distribution?

- the scale factor, σ2, is genearlly small compared to the mean so little precision is lost

- allows for probability mass function (p.m.f.) at zero which mean there can be cases where no change in loss is seen

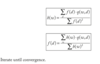

Clark: What is the liklihood estimator of the Poisson distribution?

MLE = Σci * ln(ui) - ui

Clark: What is the formula for the Cape Cod Ulitmate?

ELR = ?

Clark: What is the formula for the LDF ULTi?

Clark: What is an advantage of the maximum loglikelihood function?

- it works in the presence of negative or zero incremental losses

- since its based on expected incremental development and not actual

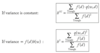

Clark: What is the total variance of the reserves?

Total Variance = ?

- Total variance is the sum of the process variance and the parameter variance

- Due to the complexity of the parameter variance, it should be given to us on the exam

Process Variance of R = σ2ΣµAY;x,y

Clark: What are the key assumptions of the stochastic reserving model?

1. Incremental losses are independent and iid

In context of reserving:

- independent means one period does not affect surrounding period

- could see positive correlation if all periods are equally impacted by change in loss inflation

- could see negative correlation if large settlement in one period replaces a stream of payments in later periods

- identically distributed assumes the emergence pattern is the same for all accident years (over simplified assumption as mix of business changes would impact this)

2. The variance/mean scale parameter, σ2, is fixed and known

- simplifies the calculations

3. Variance estimates are based on an approximation to the Rao-Cramer lower bound.

- do not know the true parameters so this is an approx.

Clark: Set up the table needed to solve for the reserves.

LDF Method

Clark: Set up the table needed to solve for the reserves.

Cape Cod Method

- MAKE sure to calculate the ELR PRIOR to truncation!

- have to do it this way as per Clark to get the right answer

- parameters will be different since on-level premium is needed so lag factors differ from LDF method

- add a column for OLP

Clark: How do you determine the process variance of the total reserve?

Just multiply the reserve by the scale factor, σ2

Clark:

rAY;x,y =

What are you looking for when examining the residual plots?

- We want the residuals to be randomly scattered around the zero line

- Can plot the residuals against a number of things to test the model assumptions such as:

- Increment Age (i.e. AY age)

- Expected loss increment - good for testing the variance/mean ratio is constant

- Accident Year

- Calendar Year - to test diagonal effects

Clark: Once the MLE calculations have been completed, there are other uses for the statistics besides the variance of the overall reserve. What are 3 uses?

1. Variance of the Prospective Loss

- Must use Cape Cod for this as we already have the MLE of the ELR

- Can use this to estimate the expected loss if we already have future premium (from budget)

2. Calendar Year Development

- This is AvE as we can estimate the development for the next CY beyond the latest diagonal.

- Good reason for this is that the 12-month development is testable within a short timeframe. One year later we can compare it to actual development and see if its in the forecast range.

3. Variability in the Discounted Reserves

- lower CV as the tail has the greatest process variance but it also gets the deepest discount

Clark: Variance of the Discounted Reserves

Rd = ?

Var(Rd) = ?

Clark: How do you calculate the estimated reserves for partial periods on an AY basis?

- must multiply the Expos(t) by G(x)

- e.g. if its September then the current year will have Expos(t) = 0.75 and G(4.5) and then you would multiply this together to get the adjusted G(x)

- for years not in the first 12 months, the Expos(t) factor is 1

Mack (1994): Mack Chain Ladder Assumption 1

Mack Assumption 1

Expected losses in the next development period are proportional to losses-to-date

E[Ci,k+1 | Ci,1,…,Ci,k] = Ci,k * LDF

- The chain ladder method uses the same LDF for each accident year (volume weighted average)

- Uses most recent losses-to-date to project losses, ignoring losses as of earlier develoment periods