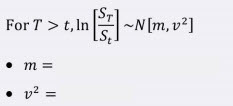

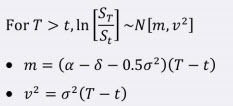

1

Q

What is the mean of the lognormal distribution, E[Y]?

A

E[Y] = em+0.5(v^2)

2

Q

What is the Variance of the Lognormal Distribution, Var[Y]?

A

(E[Y])2[ev^2-1]

3

Q

A

4

Q

E[ST|St] = ?

A

E[ST|St] = Ste(α-δ)(T-t)

5

Q

Var[ST|St] = ?

A

Var[ST|St] = (E[ST|St)2(ev^2-1)

6

Q

ST = ?

A

7

Q

Median =

A

Median = Ste(α-δ-0.5σ^2)(T-t)

8

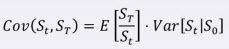

Q

Cov(St, ST) =

A

9

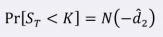

Q

Pr[ST < K] = ?

A

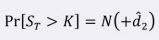

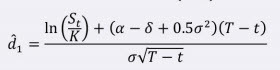

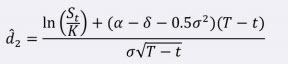

10

Q

Pr[ST > K] = ?

A

11

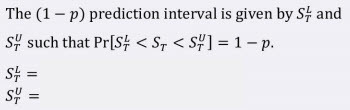

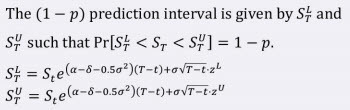

Q

A

12

Q

A

13

Q

A

14

Q

A

15

Q

Express zU in terms of zL

A

zU = -zL

16

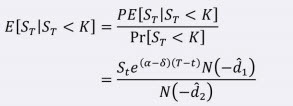

Q

E[ST|ST < K] = ?

A

17

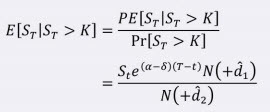

Q

E[ST|ST > K] = ?

A

18

Q

E[Call Payoff] = ?

A

19

Q

E[Put Payoff] = ?

A